Maritime trade in the ASEAN region

ASEAN as a region is the bridge connecting the Indian Ocean Region & Asia-Pacific Region. In ancient past, it was the Austronesian trade route which later became part of Chinese maritime silk route and from the side of Indian Ocean, there were long-established trade linkages among the habitants of Indian Subcontinent and the South East Asian people. Later on, the region became a junction for the flourishing trade from Europe to China. Be it then or today, the two unchanging facts being, firstly, the Indian Ocean was, is and will always have the highest traffic of maritime trade and secondly, South East Asia will always remain central to the trade through the Indian Ocean and Asia-Pacific. Even with the centrality, always the powers outside the region have had a larger say in the maritime trade of and from the region, and the ASEAN is trying to deal with it by trying to create a cohesive and single shipping market. This brings us to the question, what is the status of maritime trade of the region? This article analyses the trajectory of the same with the help of some credible statistical analysis and putting it in the perspective of current scenarios in Indo-Pacific.

The Colonial Period

The intra-regional and inter-regional trade in South East Asia had developed its linkages further during the colonial period. The pre-Modern and till the end of the colonial period saw the development of four spheres of trade linkages. Ryuto Shimada portrays these four spheres by taking the example of Batavia, Dutch East Indies (an area corresponding to present-day Jakarta, Indonesia), the four spheres are as follows:

- Long-Distance Trade: The Netherlands, Europe and the USA.

- Intra-Asian Trade: Japan, China, Siam, India and Persia,

- Regional Trade: Ambon, Bali, Bima, Bamjarmasin Palembang

- Coastal & Inland Trade: Semarang, Surabaya, Ommelanden, Priangan

Although this analysis is based on the colonial holdings of the Dutch, similar spheres existed for other colonial powers and thus the above division quite vividly encapsulates the working of the maritime trade. The profits were accrued by the European Imperial overlords; thus, the region saw a lot of trade and commerce activities without the profits being visible through material and infrastructural development of the region. The things changed in the second half of the 20th century with the sprouting of sovereign states in the region as well as the establishment of regional co-operation forum, ASEAN (Association of South-East Asian Nations).

Maritime Trade | The driver of ASEAN success story

Latest statistics:

China (17.2%), EU-28 (10.2%), and USA (9.3%) are ASEAN’s top three trading partners in 2018. The largest external markets for ASEAN exports in 2018 were China (13.9%), EU-28 (11.2%), USA (11.2%), and Japan (7.9%) with total exports by goods by ASEAN member nations being US$ 1,436,415.0 million. Intra ASEAN trade being at 24.1% of the total trade in the region.

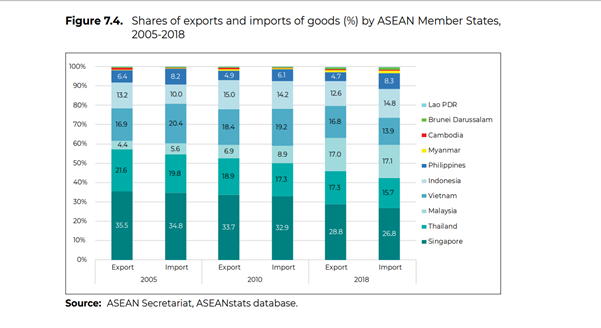

The above graph provides the country-wise share of exports in the overall US$ 1,436,415.0 million exports from the region. The observation in ASEAN Statistical Year Book 2019 goes, “As a trade hub, Singapore was the largest exporter in the region in 2018, with a share of 28.8% of the ASEAN total exports, followed by Malaysia (17.3%), Viet Nam (17.0%), and Thailand (16.8%). As for imports, similarly, the largest importer being Singapore with a share of 26.8% of ASEAN total imports, followed by Viet Nam (17.1%), Malaysia (15.7%), and Indonesia (14.8%). Exports and imports shares in ASEAN’s total significantly increased for Viet Nam from 4.4% and 5.6% in 2005 to 17.0% and 17.1% in 2018, respectively. Myanmar, Cambodia, and Lao PDR also observed increases over the same period.”

The two observations which can be made out of these stats are: first, the maritime states in ASEAN can capitalize on the need of manufacturing centres as they can provide cheap labour, infrastructure for production and transportation outpost being in a nearby vicinity; these features and many others have had a tremendous impact on the moulding of maritime states as manufacturing hubs. Second, because of the rise of these maritime nations in ASEAN has also provided avenues for the mainland ASEAN nations for catalyzing their economic development. The increase in the export and import share of Myanmar, Cambodia and Lao PDR are obvious examples how the growth of the maritime nations as the transportation & shipping hubs has had a positive impact on the economies of mainland South-East Asian States.

ASEAN Maritime Transport & Roadmap for its future

From the very formation of the ASEAN Maritime Transport Cooperation, the member nations are keen to develop a single ASEAN shipping market for goods and services by promoting progressive liberalization of maritime transportation. This will objectively improve the region’s maritime performance and international competitiveness by providing quality services at competitive pricing (which has become the hallmark of the region).

Roadmap

As per the report on “Promoting Efficient and Competitive Intra-ASEAN Shipping Services” by PDP Australia Pty Ltd/Meyrick and Associates published in March 2005 elaborates, “The liberalization of transport services is consistent with and supportive of the commitment of the ASEAN Leader’s commitment, recorded in the Bali Concord of October 2003, to the development of ASEAN as a single market and production base. Specifically, it furthers the goal of the leaders to institute new mechanisms and measures to strengthen the implementation of its existing economic initiatives, including the 1995 ASEAN Framework Agreement on Services (AFAS), and supports the goals and strategies enunciated in the Transport Sectoral Action plan 2005-2010.”

The measures which were undertaken can be grouped in 5 key themes, namely;

- Developing a single ASEAN voice: Building capacity for the ASEAN to express a single coherent policy position on maritime matters of common interest to ASEAN countries.

- Infrastructure: Making sure that transport infrastructure exists to support the effective and efficient operation on intra-ASEAN shipping services.

- Integration: Development of a single integrated ASEAN shipping market in which all ASEAN operators can operate without restriction.

- Harmonization: Ensuring the competition takes place on equitable terms and conditions.

- Human resource and capacity building: Developing and spreading throughout ASEAN the management capacity and technologies required to manage shipping and port operations safely, efficiently and in an environmentally acceptable manner.

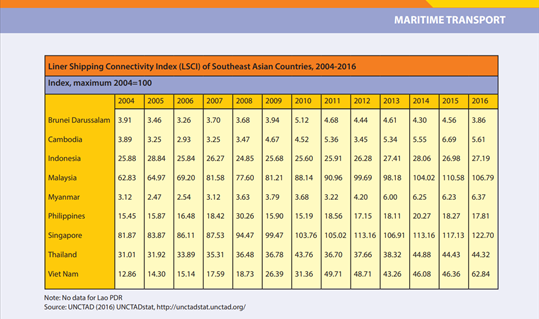

As for the implementation part, it is heartening to observe that for more than 12 years now the intended cooperation within ASEAN has been progressing well. As the ASEAN transport development, 2017 report observes “The Liner Shipping Connectivity Index Statistics of UNCTAD shows that from 2004 to 2016, ASEAN has reached steady progress in terms of its connectivity to global liner shipping networks, which also indicates the region’s better access to the global trade.”

The above table of UNCTAD data on LSCI captures the level of integration with the global shipping network. The increased number of ships calling at ASEAN ports indicates an upward trend of import, export and transhipment activities in ASEAN which would sustain trade in global markets.

Threat of COVID-19

The task was achievable and steps were being taken towards it, however, the COVID-19 pandemic did not just put roadblocks in the path, but in many ways, it is reversing the milestones ASEAN nations had achieved. The equitability which we were talking about can only be achieved if the states have a certain required level of capacity for sustaining the shipping industry equitably and maintaining the competitive pricing and quality simultaneously. The COVID-19 pandemic has forced states to look inward, prioritizing their internal challenges instead of the multi-national organizational duties & obligations. This has jeopardized the capacity building efforts and can have cascading effects in retrospect.

What’s Ahead?

A ray of hope is that, though all other indices are plummeting, ASEAN can maintain the volume & intensity of intra-ASEAN trade. In addition to this, the demand from the People’s Republic of China is increasing after a steep fall. Thus, things can pick up if no further slump is in stock for us; the goods & services which were to be exported to European Union and the USA will observe a steady fall, however, if South-East Asian nations stick together and work towards minimizing the impact on the progress of Maritime Cooperation, then with very little delay, a stronger and cohesive ASEAN will emerge.