Analysis: Ukraine may prove wild card for inflation-obsessed markets

With surging inflation and central bank policy occupying investors’ minds, the traditional market playbook on how to react to military flare-ups has been thrown out of the window.

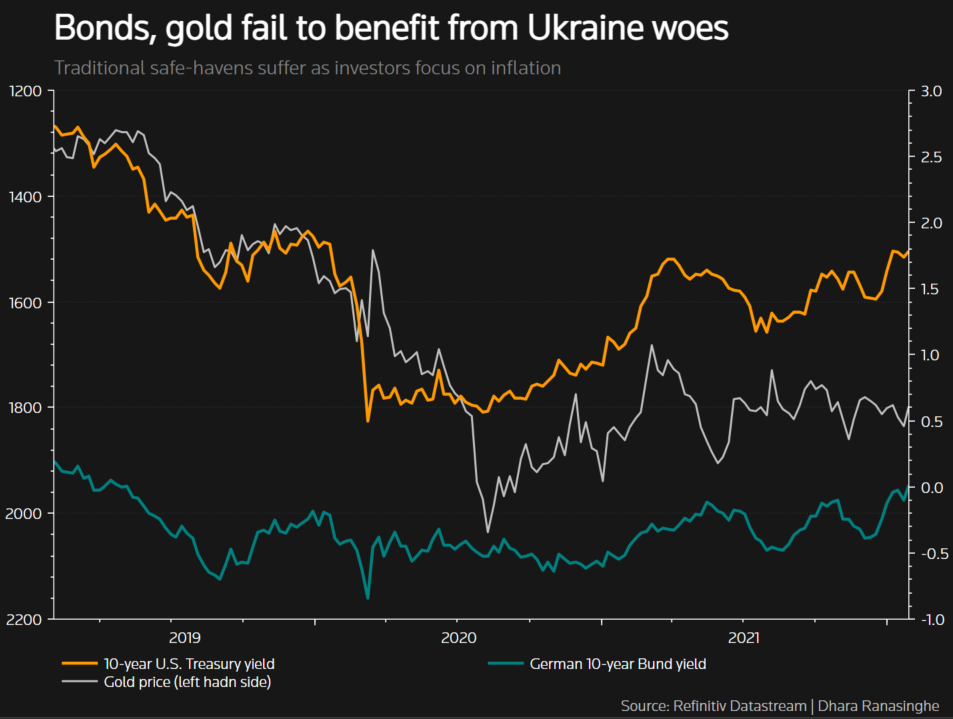

Unease over Russia’s troop build-up near the Ukraine border contributed, alongside U.S. rate-hike jitters, to a 5% slide on Wall Street last month. Yet top-rated government bonds and gold, assets that typically rally when political upheaval or war threaten, failed to benefit.

U.S. and German bonds – considered the safest assets of all – witnessed their worst month since early 2021, with yields surging 30 and 20 basis points respectively , as inflation and the prospect of higher interest rates commanded the spotlight. Gold fell 2% .

It isn’t often stocks and bonds fall at the same time. John Briggs, global head of desk strategy at NatWest Markets, estimates this has happened in 35 months since 2000 – or roughly 14% of the time.

The inverse correlation between equities and bonds has long been relied on by investors to safeguard returns in times of trouble, with a 60:40 portfolio split one traditional strategy.

Now though, Briggs says investors “need to entertain the idea” that markets could react differently when central banks are focused on responding to higher inflation.

“If we do see a further deterioration in the Ukraine situation, for investors looking for traditional safe havens, some of the old correlations may not hold.”

Markets’ muted reaction to Russian sabre-rattling – it denies it is planning to invade its neighbour – may not come as a surprise to those who note that recent risk events, from missile launches to attacks on Gulf oil facilities, have had only a fleeting impact on investment behaviour.

What’s different this time is that inflation, subdued for decades, is running hot in many countries. Conflict with Russia would further fan inflation fears by boosting oil and food prices.

John Flahive, head of fixed income investments at BNY Mellon Wealth Management, said recent market volatility had left his clients a “bit unsettled”.

“Normally if you see an equity market that’s down 10%, you’d see some flight to quality in your higher-quality fixed income securities and that’s really not happening,” he said.

“So you wake up at the end of January, and there really aren’t many portions of your portfolio that have been insulating, and everything is red.”

A typical 60:40 portfolio was down 3.77% in January after a 2.34% rise in December, said Vincent Chaigneau, head of research at Generali Investments, although still up 5.3% from the end of January 2021.

Policymaker Headache

For policymakers trying to exit pandemic-era stimulus and contain inflation, the military threat is an added complication.

The Federal Reserve will likely start raising rates in March, the Bank of England is tipped to hike for the second time in as many months on Thursday and record euro zone inflation could force the European Central Bank to reassess its view that price pressures are temporary.

One question is whether brewing political risks are simply flying too far below the radar for inflation-obsessed markets. But if the tried and tested bond hedge fails to deliver, what options do investors have?

One portfolio manager said clients are increasing exposure to investment grade corporate debt, seen as a stable source of returns.

Investors might also make a beeline for the dollar and other U.S. assets, which tend to outperform during periods of geopolitical tension.

Amundi Asset Management recommends investors stay neutral in terms of risk allocation considering constructive earnings revisions in many sectors, but be ready to reduce risk should the situation materially deteriorate.

Repricing

If tensions escalate and markets reprice expectations for the growth outlook and monetary policy response, safe-haven bonds could yet get their allure back.

Europe’s reliance on Russian gas makes it particularly vulnerable.

BofA analysts estimate that in an extreme scenario, Brent crude could rise roughly 30% from current levels and natural gas prices could jump 200%, lifting the bank’s forecast for headline euro area inflation this year to 4% from 3% but cutting its current GDP forecast of 3.6% by 50 basis points, which would leave the ECB scant room to hike rates.

For Randy Kroszner, a former Fed Governor and now an economic professor at the University of Chicago Booth School of Business, Ukraine could prove a geopolitical test case for markets.

“That’s one of the wildcards that we certainly haven’t had in recent years — moving from a cold war to a hot war that could involve Russia and NATO,” he said.

Reporting by Dhara Ranasinghe; additional reporting by Sujata Rao; Editing by Sujata Rao and Kirsten Donovan