Ayushman Bharat: Humbug of Universal Healthcare

Introduction

In 2015, the first year of the Modi government, New Health Policy was launched. The aim of the New Health Policy was not to increase the spending on healthcare but to emphasize the role of private healthcare organizations. This New Health Policy was different from the health schemes of the government of India, which focused on supporting public health goals to achieve a reduction in child mortality rates. 15 National Health programs including those controlling the tobacco use elderly care were merged with the New Health Policy scheme. Following the trends observed after the launch of this policy, the funds received were seen to fall in comparison to 2015. Hence, the government of India developed a draft policy to introduce a universal healthcare system, known as the National Health Assurance Mission. Under this plan, the government was to provide free drugs, diagnostic treatment, and insurance coverage for serious ailments, although budgetary concerns delayed its implementation. The government announced, “Ayushman Bharat” (National Health Protection Mission or Pradhan Mantri Jan Arogya Yojana) in 2018 Union Budget of India. (when fully implemented, It will be World’s largest health protection scheme).

The scheme is divided into two parts, the first aims to create 150,000 health and wellness centres (HWC) to cater to the primary healthcare needs and the second is dedicated to providing health insurance for secondary and tertiary healthcare. Being hailed as the largest public-funded insurance scheme, it aims to provide financial protection to the weak and vulnerable as out of pocket expenditure (OOP) is considered to be one of the biggest factors to drive people into poverty. The state governments can implement the scheme in either of the two forms, Insurance model or trust-based model. The households who qualify for the scheme will be insured for a total sum of 500,000 per family per annum. The scheme doesn’t put a cap on the number of family members and covers both pre and post hospitalization charges. The financing of the scheme will be shared in a 60:40 ratio between centre and state. The beneficiaries will be identified as per the socio-economic caste census (SECC) of 2011. When the scheme will be fully implemented, it has been estimated to cover over 10 crore households. In 2019, the budget allocation for the scheme was Rs. 1,600 crores ($210 Million) for HWC’s and Rs. 6,400 crores ($837 Million) towards insurance.

The objective of this article is to critically analyze the challenges to the scheme and the effectiveness of target-based insurance to achieve universal healthcare.

The Policy Conundrum

The most basic question that arises before we go further is what are the challenges in road to universal health coverage under the current system in India?

Healthcare is not an isolated concept thus any policy aiming at universal coverage catering to a huge population can’t be carried out in solitude. Various factors come into play to implement and sustain a massive policy as this one.

Economic

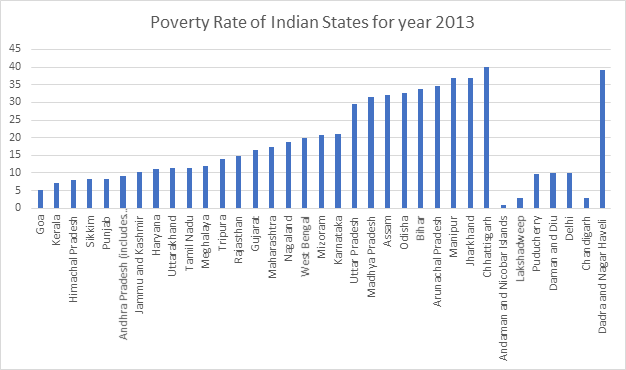

One of the biggest challenges to the scheme is finance. Even a 5% claim rate at an average claim amount of Rs. 30,000 ($292) would require around twice the amount of current budget allocation to the scheme. The fact that the states have to bear around 40% of this burden adds to the misery as the states with high poverty does not have any sustainable sources to fund it. Central Government’s commitment to keeping a check on its fiscal deficit along with the state government’s inability to set its GST rates exacerbates the problem. According to the scheme, if the state government wants to include a particular caste or community in the beneficiary list, it can do so but only at their own cost. A study of some of the poorest states in terms of GSDP and tax revenues and the percentage of the population living under poverty reveals that the majority of the poor states lack the necessary funds to finance their share of the scheme.

Looking at the graph above, the states with the lowest GDP also have a high proportion of the population living under poverty. According to government data, Bihar and North Eastern states have been the worst performers under the scheme. This reinforces that poor states are facing difficulty in properly implementing the scheme. The other issue related to financing is wasteful expenditure. For the insurance claim settlement, the government has decided that the insurers will be required to return a share of the premium collected from the government for failing to satisfy a healthy claim ratio. In case of a claim ratio of under 85%, the insurer can hold a maximum of 15% of the unclaimed premium and return the whole to the government. This requires the government to have a strict check on the insurance companies for bogus clients, which is a lower-middle-income country like India is a very difficult process. The wastage of funds in terms of administrative costs leads to inefficient allocation of resources, data from state insurance schemes support this claim where the governments have spent more than Rs. 2,300 crores ($300 Million) to get a benefit of Rs. 1700 crores ($222 Million), which boils down to Rs. 0.7 ($0.0092) worth of benefits per Rs. 1 ($0.013) spent on premiums. In the case of the trust model, the state government sets up a trust to perform the role of an insurance company and the government fixes the price, hence there is no price discovery. In the insurance model, the state floats a tender and the insurance company is selected based on the ensuing bidding process. The fact that most states governments have gone with the Trust based model, shows they are themselves sceptical of the insurance companies.

Social/ Educational:

Another problem is the myopic view of the government to analyze the situation, providing insurance only deals with the demand aspect of healthcare, what the government must realize is the fact that there are supply-side issues to healthcare that remain unresolved and that these issues account for poor health outcomes. By 2030, India will need 20.7 lakh (2.07 million) doctors to reach a doctor population ratio of 1:1000. This implies a growth rate of 151% registered doctors in the country, given the past 5-year growth rate of a mere 14.4 % the warranted growth rate is simply unachievable. The severe lack of social infrastructure like hospitals in rural areas is a major problem that needs to be resolved. According to a WHO survey, the number of beds per 10,000 is merely 9 in India.

The biggest issue of all is the problem of implementation of this free cashless health insurance. The major issue with implementation is the fact that people lack awareness about the facets of the scheme. Over 1 year of implementation of the scheme, 46.4 lakh (4.64 Million) have received the treatment through hospitalization while many patients have been declined the treatment based on the type of illness. Many big corporate hospitals have chosen to stay away from the scheme because they believe that the scheme is non-viable and that they won’t be able to meet the costs if they met the treatment at prices that the scheme demands.

Political/Ethical

India is a federal country, the delivery of healthcare largely rests with the states, health being a state subject. Considering the political skirmishes, states like Delhi, West Bengal, Odisha, Kerala, and Telangana have kept an arm’s length from the scheme thus not allowing the scheme to be implemented pan India, as the states having their health care system which according to them is catering to a larger population in their states than what PM-JAY would cover.

Corruption is another issue when it comes to operation and functioning of the scheme because within one year the scheme has observed a good number of frauds associated with the monetary health cover that it promises. Other than that, Information technology provides a robust backbone to the scheme’s implementation throughout the country but the lack of basic internet facilities has become a major hindrance for some of the states.

The other problem that arises is that of information asymmetry and moral hazard. As naturally, the doctors would have more knowledge than the patients, they may use this asymmetry to pocket the public money. Even though the data under the current scheme isn’t available, Treatment under various state insurance scheme data from Maharashtra (MPJAY) and Karnataka backs this theory. The most expensive packages under the schemes are cherry-picked by the private hospitals leaving the not so profitable ailments to the public sectors. the tables below prove our hypotheses, the treatment packages that are the most expensive are also higher in terms of treatment.

Having an insurance cover and not paying anything for it causes the problem of moral hazard on the patients’ side. Where they don’t take the necessary precautions to keep themselves healthy. According to Friedman’s law of spending, when a person spends someone else’s money on himself, he cares more about the quality than the cost which would lead to unnecessary tests and surgeries that may be avoidable under normal circumstances. Many cases of fraud and impersonation have already been registered with the police and a large number of non-beneficiaries have been able to use the insurance benefits. The problem exacerbates as most of the hospitalization payments are in the form of reimbursements and there have been cases of no or delayed reimbursements adding to the misery of the poor.

Environmental

A substantial burden of diseases in developing countries like India is attributed to environmental factors. A healthy environment is needed for sustaining a healthy population, around 1.3 crore (13 million) deaths occur per year around the world due to preventable environmental causes related to water, hygiene, sanitation, harmful use of chemicals, indoor-outdoor pollution and climate change. Deteriorating surface and groundwater quality is one of the most serious environmental problems for India, this is accentuated by urban air pollution, and increased risk of climate changes causing many diseases like lung and skin cancer, brain disorders, etc. Almost 85-90% of the patients have waterborne diseases, malnutrition, malaria, typhoid and these are not what PM-JAY addresses.

The impact of environmental degradation on health is likely to get worse in the future unless action is taken urgently.

Environmental risk factors and the diseases contributed

| Risk factors | Related Diseases |

| Water, Sanitation | Diarrhoeal diseases, trachoma, hookworm disease |

| Indoor Air Pollution | Pneumonia, COPD, lung cancer |

| Outdoor air Pollution | Respiratory infections, cardiopulmonary disease, lung cancer |

| Arsenic | Dermal keratosis, cancer |

| Climate Change | Diarrhoeal diseases including cholera, malaria and other vector-borne diseases, asthma, COPD, malnutrition |

Lessons to be learnt

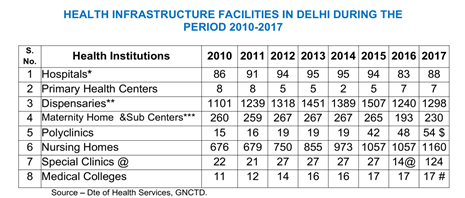

A Case Study: Healthcare System in New Delhi

Delhi is the national capital and has a population of around 2 crores (20 Million) of which 97.5% population lives in urban areas. There are twelve different agencies providing healthcare in the city currently. The current government in Delhi has done unprecedented work and has been globally applauded for making quality healthcare affordable and accessible to the people of Delhi. The government has allocated 12.7% of its budget for healthcare for the financial year 2019-2020.

New Delhi has a three-tiered network of Mohalla clinic, Polyclinic, and Hospitals which through different schemes launched by the government helps in providing free medicines, tests, and several life-saving surgeries.

Mohalla clinics: There are 158 Mohalla clinics to provide free healthcare services through a healthcare facility at a walking distance, assured availability of primary healthcare, medicines and diagnostic tests, the targeted population of mohalla clinics are the migrants, undeserved, jhuggi-jhopdi colonies, each serving around 10000-15000, population.

Polyclinics: The government has launched 23 polyclinics specialized in providing diagnostic tests and treatments to the population helping in reducing the out-patient burden on hospitals and making it more accessible.

Hospitals: 38 fully-fledged hospitals fall under the purview of the Delhi government, all medicines, tests, and surgeries at these hospitals are completely free of cost. If a resident of Delhi is waitlisted for a life-threatening disease surgery for more than 30 days he/she can go to any empanelled private hospital and can get the surgery done for free, there are around 52 surgeries which patients can avail for free of cost.

The GOI must learn from the state government of Delhi, which has impacted the lives of the poor through its mohalla clinics and has garnered rave reviews from international personalities like Kofi Anan. Jon Dreze and Amartya Sen have warned the government of using target-based insurance schemes for universal healthcare because it is inadequate and may lead to a rise of an insurance lobby which will make it impossible to dilute the scheme in the future.

One Year Policy Analysis of PM-JAY

Till now 32 states and union territories have implemented the scheme, in the last one year free secondary and tertiary treatment of worth Rs. 7.966 crores ($1.04 Million) have been availed by people and more than 50 lakh (5 Million) treatments under PM-JAY have been done. The tertiary treatment\s accounts for more than 60% of the treatments

The top-performing states are Gujrat, Tamil Nadu, Chhattisgarh, Kerala, and Andhra Pradesh.

PROGRESS OF PM-JAY (as on October 17, 2019)

E-Cards Issued: more than 10.9 crores (109 Million)

Beneficiaries Admitted in Hospital: More than 50 lakh (5 Million)

Amount Authorized for Admissions: More than Rs. 8000 crores ($1.04 Billion)

Hospitals Empanelled: 18,552

Suggestions

There is a lot that can be done and needs to be done, be it under this scheme or for a robust healthcare system in general.

The Government of India can learn a lot from the south Indian states in terms of healthcare delivery, the performance of south Indian states has been evidentially better than all India.

There is a long-time pending need for a substantial increase in public healthcare expenditure which is a meagre 1.28% of the GDP. There is an urgent need to save and strengthen the public healthcare sector making it more inclusive and accessible. The government should work on more comprehensive policies for affordable and accessible medicines targeted at reducing the out of pocket expenditure of the people. The need for effective regulation of the private sector in medical to ensure patients’ rights and avoid exploitation of patients at the hands of private hospitals also needs to be addressed. Stringent laws and action to curb the medical malpractices and to fight corruption in the public healthcare system require more attention from the government. Special attention to women’s health rights and gender equality through policy intervention can be done. The quality and affordability under PM-JAY need to be kept under constant scrutiny, no compromise with the quality of healthcare offered should be tolerated. Linking of PM-JAY with primary healthcare can help in yielding better results there is a need to strengthen the IT and anti-fraud infrastructure working under this scheme, and for the scheme to be more effective more and more empanelment of hospitals needs to be done. Environmental awareness and its importance to curb many diseases need to be highlighted. And most important of all there is a need for a robust network to spread across the information and ensure last-mile delivery, this is not possible without an extensive awareness network in place.